The Illusion of Certainty & Search for Clarity - I

Dear Clients,

Wishing you a Happy & Prosperous New Year. Hope you are in the pinkest of your health.

Now that we are back to Pre Covid levels on the main indices (Sensex / Nifty), one question that is lingering on my mind and of course on yours as well is this. Is this the near term (2,3,6 months) peak? Or can the markets go higher than where they are today in the next 2,3,6 months? My answer is not “Neat”. In other words I cannot say with “Certainty” that it will be higher than where it is today, but I can say that the “odds” for the markets to be higher than today in next 6 months are higher, especially the broader markets. Please go back to the previous sentences and look at the words that I have “quoted”. Neat, Certainty, Odds. I want to talk about these seemingly simple words and how they shape our thinking. Let us start with the word Neat.

The moment an analysis is put on paper, it becomes “Neat”. And we all like Neat things. To put an analysis on paper we need to put numbers. What this does is, it gives an Illusion of linearity. Here is an analysis I did on Ashok Leyland some time back (Aug-Sep 2019). I said that at the current market capitalization of 18,000 crores the stock seems to be undervalued and one should buy it. The assumptions were that Free Cash Flows will grow at 10% per annum. In turn margins will hold at whatever levels they have been for past several years, Sales growth will be there etc. Today the Market Cap of Ashok Leyland is more than 26,000 crores a growth of around 50% but Sales are down, Margins are down and FCF is negative for the last year.

|

Year |

FCF |

Growth |

Present Value |

|

|

1 |

2,110 |

10% |

1,835 |

|

|

2 |

2,321 |

10% |

1,755 |

|

|

3 |

2,553 |

10% |

1,679 |

|

|

4 |

2,809 |

10% |

1,606 |

|

|

5 |

3,089 |

10% |

1,536 |

|

|

6 |

3,398 |

10% |

1,469 |

|

|

7 |

3,738 |

10% |

1,405 |

|

|

8 |

4,112 |

10% |

1,344 |

|

|

9 |

4,523 |

10% |

1,286 |

|

|

10 |

4,976 |

10% |

1,230 |

|

|

|

|

|

|

|

|

Final Calculations |

|

|

|

|

|

Terminal Year |

5,075 |

|

|

|

|

PV of Year 1-10 Cash Flows |

15,145 |

|

|

|

|

Terminal Value |

9,650 |

|

|

|

|

Total PV of Cash Flows |

24,795 |

|

|

|

|

Current Market Cap (Rs Cr) |

18,758 |

|

|

|

Then why did the stock go up? From last year when I did the analysis it is up by about 50% and since the low of Covid related market crash of March 20, it is up by 100%. There are some good reasons behind that, but they are not as Neat as I put them on paper. It is one of the largest truck manufacturers in India and amongst Top 10 in the world. It has the highest market share in the segments that it operates in. It is well managed and unlike it’s close competitor TATA, it is focused only on heavy commercial vehicles. These things cannot be neatly described through numbers. Over and above that markets are forward looking. So, if the franchise is strong the market may be willing to excuse the poor numbers for a year or two, especially in times like Covid. Analysis is important. One need to have a framework and numbers in their heads and on paper. But in real life things are not as Neat as they seem to be on paper. So always be careful about all those Neat analyses that you see in presentations. What a Neat analysis does is that it gives us the Illusion of Certainty. Let us see how it happens and why it is dangerous.

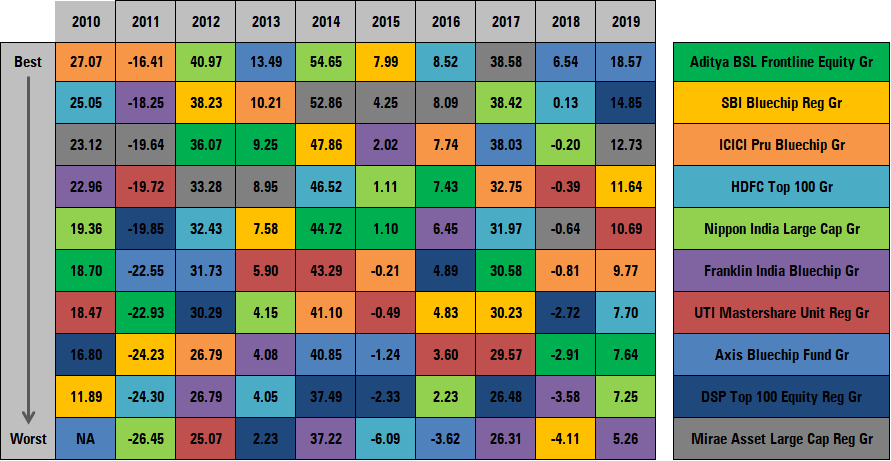

One of the most frequent things I have heard from investors is why did we invest in fund A and not Fund B? If I ask them why Fund B, the answer is, you all guessed it right, last 1,3,5 year returns are good. We don’t comprehend the mathematics behind this. If last 1- or 2-year returns have been good, it will indirectly make last 3 and 5 years returns good as well and vice versa for bad return. We conclude “only and only after it has happened”. Once it has happened it is certain, right? But that is the past and not the future. We are not going to benefit from past return but from future returns. If I ask another question to the same investor, what is it that you like about the Fund B, other than the return? Again, you guessed it right. They don’t have the answer. If you and me can open a website and see the best performing funds, I am sure other people can do that as well, isn’t it? And if that is how people can make money, everybody would be a billionaire by now. Isn’t it? Here is an interesting chart that I pulled out from Morningstar website.

It shows the best performing large cap funds from 2010 till 2019. If you see you will notice that not a single fund has been consistently on the top for 3 years in a row. At best ICICI Pru Bluechip was a best performing fund in 2010 and 2011 but if you see in last 3 years, it is not even in top 3. The fund is not bad. It’s the cycle through which all the funds go. Currently Axis shows up as the best performing fund, but it was nowhere near the top in 2014, 2015. Again, it is not a bad fund. Just goes through a cycle.

It shows the best performing large cap funds from 2010 till 2019. If you see you will notice that not a single fund has been consistently on the top for 3 years in a row. At best ICICI Pru Bluechip was a best performing fund in 2010 and 2011 but if you see in last 3 years, it is not even in top 3. The fund is not bad. It’s the cycle through which all the funds go. Currently Axis shows up as the best performing fund, but it was nowhere near the top in 2014, 2015. Again, it is not a bad fund. Just goes through a cycle.

So, the strategy that an investor uses (looking at the past returns after they have happened) is bad. If an investor uses that strategy consistently, he is bound to fail. Everybody can go to a website, look at the past returns and say this is “THE FUND”. I REPEAT, EVERYBODY CAN DO IT. A mortician or a coroner who does a “postmortem” is not paid as highly as a surgeon who does a surgery on some who is alive. Why? Because postmortem is easy. Surgery on an alive person is not. Coroner doing postmortem will “NEVER” make a mistake because the person is already dead. A surgeon can and will make a mistake but still he will be paid more. Much more. Past performance after it has happened, and Neatly shown in a table gives us the sense of Certainty. That is not Certainty. It is an Illusion of Certainty. The moment I took a Life Insurance Policy, I implied to myself that Life itself is uncertain. If I look around myself and think about things I used to think or believe in last 3, 5, 7, 10 years, I know that life is uncertain. Lots of things never panned out the way I thought and some of them never panned out. So, if Uncertainty is always there what should we look for? The answer is Clarity.

Clarity in investment (or any other field) is understanding that there is uncertainty and to deal with that uncertainty we must think in terms of “Odds”. Yes, we must think in terms of probability of the event happening and / or not happening. We have to think what are the odds that market will be higher than today after 6 months? Why? If the odds are in our favor we act. If they are not, we don’t. Because our brain likes things that are Neat & Certain, we tend to look for evidence that conforms our beliefs and then jump to conclusions that the event in question is a certainty. No, it is not. I know thinking in terms of probability is hard but that does not mean that we take an easy route and declare every event as a certain event, especially after it has already occurred.

It is hard to believe that markets can go up for a long time, because last 2 and a half, almost 3 years have been hard for us and our brain is not able to comprehend that markets can go up substantially. The same things happen in a bull market, albeit in an opposite fashion. We are not able to comprehend that markets can fall and remain fallen for a long period of time. Today the anxiety is markets have reached all-time high, it should fall today, if not today tomorrow, if not tomorrow day after and day after. Until the market falls, we will remain anxious. Because that is what we want today. Because that is what we have seen in last 2 and half years. Exactly opposite happens in bull markets. Markets will fall tomorrow, I know, but it will recover day after tomorrow so there is no point in getting out of the market. There is no anxiety about markets going up in bull period and a correction is seen as a buying opportunity. Only after a prolonged or a sharp correction, people start thinking about a bear market possibility. In the same manner, coming out of the bear market, only after substantial gains, people start to believe that the bull market has already started. Not initially. After a substantial upside has happened.

In my next article, I would like to present a framework to think about Odds or bringing clarity in our thought process to make sound investment decisions. Not on some hunch but based on probability and what is know and what is unknown.

Till then,

Regards,

Nishith Vyas